Dousing the Pyre

On the sovereign arson of Australian Real Estate and why a correction could lead to enormous monetisation of bad housing debt.

April 15, 2026 -

Shane Hull

Real Estate cycles are just capital cycles. We are facing a necessary deleveraging, but the Australian Government refuses to let it play out.

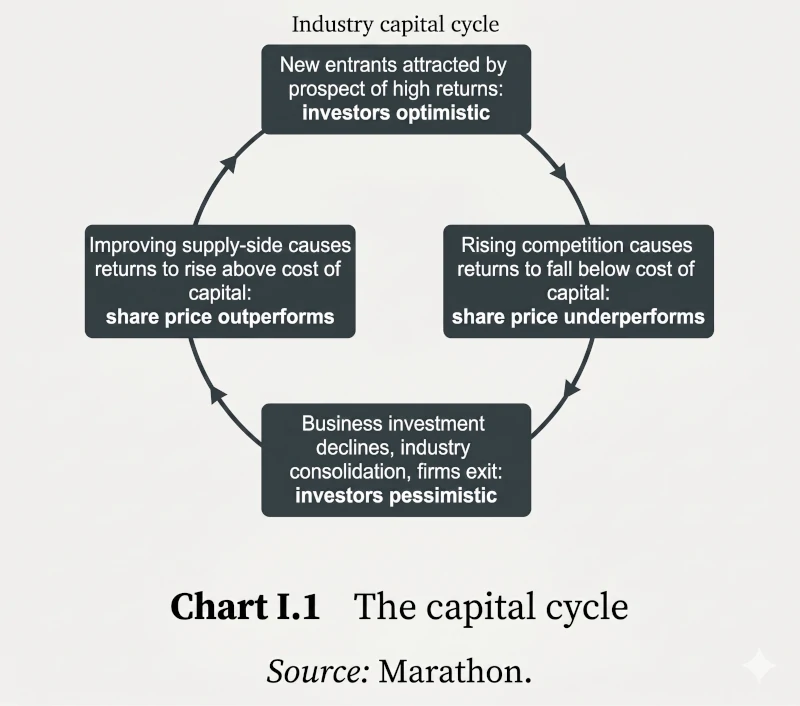

The Capital Cycle

Capital cycle theory offers a rational, bottom-up explanation of market cycles. Unlike the 18.6-year real estate cycle, it tracks how capital flows drive supply responses rather than relying on arbitrary timeframes. Crucially, capital cycles interact with debt cycles. In Australia, it’s the latter that’s being weaponised to delay the former.

Under normal capital cycle theory, the mechanics are brutal but rational:

- High property prices and strong returns attract a flood of capital.

- This capital funds a massive increase in productive supply (construction boom).

- The market becomes oversupplied, yields collapse, and prices crash.

- Capital flees the sector, supply stagnates, and the foundations for the next boom are laid.

The Australian Anomaly

The Australian housing market is stuck in a broken loop. High prices are attracting capital, but structural blockages (NIMBY zoning laws, skyrocketing construction costs, and chronic builder insolvencies) prevent that capital from generating productive new supply. In 2026, dwelling completions are sitting roughly 30% below the National Housing Accord targets.

Importantly, these supply constraints are not organic. They are artificially amplified by the same policies meant to support demand. Mass immigration has outpaced construction capacity, while leveraged buyers bid up prices faster than supply can respond. The market is supply-constrained by design.

Because capital can’t flow into supply, the government actively redirects it into demand. And in a big way.

Where Are We in the Cycle?

We are firmly in the late-stage, overcapitalised exhaustion phase of the cycle, but the downturn is being artificially delayed. The RBA’s rate cuts in 2025 gave borrowing capacity a temporary sugar hit, but inflation has flared again in early 2026. They are trapped. They cannot raise rates without crashing the housing market they propped up, but cannot keep rates low without letting inflation burn. The tail now wags the dog — monetary policy is held hostage by the very market intervention that was meant to save it. We should be entering the downturn. Instead, we are trapped in a holding pattern.

Engineered Distortion

When organic demand taps out because prices have detached from local incomes, governments have two choices: let the market clear and accept deflation (political suicide) or underwrite the debt themselves. Australia has aggressively chosen the latter.

With the 5% Deposit Scheme & Help to Buy, the government has essentially become a subprime lender and co-investor. With the expansion of the Help to Buy program, the government is taking up to a 40% equity stake in homes.

The moral hazard here is fundamentally “bad capital”. By guaranteeing these loans, the government bypasses standard bank risk modelling (which already favours property and has largely stopped lending to productive business). It funnels taxpayer money directly into the secondary market (existing homes) rather than to incentivise new builds, acting as a sovereign accelerant that simply bids up the price of existing collateral.

We should be entering the bust/deleveraging phase. Instead, the market has become a sovereign pyre; a massive, combustible structure of unproductive debt and dead capital, held upright only by state intervention. To prevent it from collapsing, the government is dousing it in the only thing they have left: more subsidised leverage.

But this distortion doesn’t raise all boats equally. It creates highly concentrated pockets of risk, confined to a particular segment and demographic.

The Segment

The “affordable” end of the market (units, townhouses, outer-ring suburban homes) is seeing the most aggressive price distortion. Because government schemes have price caps, a wall of subsidised capital is funnelled directly into entry-level stock, inflating the bottom tier of the market far beyond its intrinsic value.

The Demographic

Millennials and older Gen Z are being used as exit liquidity for the previous generation’s leveraged positions. By granting them subsidised leverage to enter a tapped-out market, the government is saddling a generation with dangerous Debt-to-Income (DTI) and Loan-to-Value (LVR) ratios that are subsidised by their own future tax dollars.

Inelasticity in a Downturn

Should the downturn overwhelm the state’s ability to prop it up, the traditional mechanisms for stabilizing the market are severely compromised, creating an inelastic response that amplifies the downside.

Foreign Capital is Sidelined

In a typical crash, cheap currency and lower asset prices invite foreign bottom-fishers to stabilize the market. However, the Australian government implemented a two-year ban on foreign buyers purchasing existing dwellings starting in April 2025. That liquidity floor is currently gone.

Hoomer Deleveraging

The Australian market is highly reliant on retail investors utilizing negative gearing. If capital growth stalls or goes negative, the carrying cost of these assets becomes toxic. Instead of buying the dip, highly leveraged retail investors (“hoomers”) will become forced sellers.

The Taxpayer as the Ultimate Bagholder

Because the government has taken direct equity stakes in the market and guaranteed low-deposit loans, a market correction means the state balance sheet absorbs the negative equity. The available capital to stabilize the market in a severe downturn will just be the central bank printing money to bail out its own bad housing bets.

We are watching the total financialisation of shelter, where the government cannot afford to let the cycle run its natural course.

But why should we be surprised? This is a feature, not a bug. The state has made housing a political asset that cannot be marked-to-market because deflation threatens their survival.

Having doused the market in bad debts, the state opens the doors to monetisation on an enormous scale, allowing them to transfer their egregious interest obligations onto the taxpayer in a sly manner. The final act of sovereign arson.